CFO Message

responding to rapid changes in the external environment,

and to build a corporate structure that can generate

sustainable profits that exceed capital cost

Executive Officer,

CFO (Chief Financial Officer) Masaaki Yamamoto

Key points of financial results for FY2024

Our Group launched the Medium-term Management Plan “DRIVE NTN100” Final in April 2024, aiming to continue “accelerated transformation to the business structure” and complete NTN's revitalization.

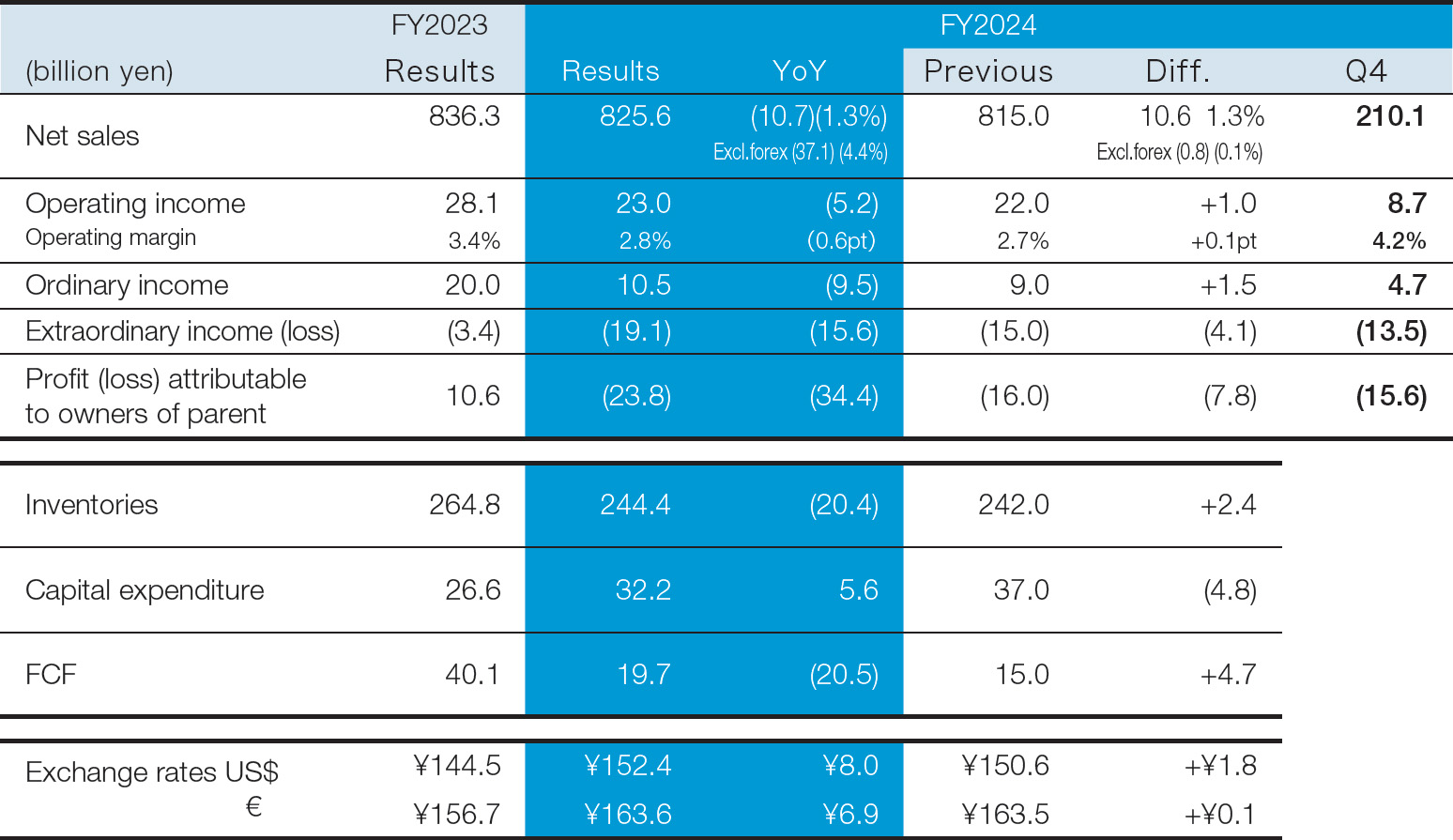

In FY2024, the first year of this plan, our Group's net sales were 825.6 billion yen (down 1.3% from the previous year) due to slow recovery in demand in the automotive and industrial machinery markets.

Regarding operating income, despite our efforts in the improvement of sales prices and cost reduction, as well as the impact of exchange rates due to yen depreciation, we were unable to offset the scale reduction, resulting in 23.0 billion yen (down 18.4% from the previous year). However, compared to our announced forecast, we achieved a 1.0 billion yen increase from the previous year. Ordinary income was 10.5 billion yen (down 47.6% from the previous year) due to foreign exchange losses and other factors. Net loss attributable to owners of parent was 23.8 billion yen, as we recorded minus 19.1 billion yen in extraordinary losses mainly due to structural reform costs, and the impact of tax effect accounting due to poor performance in the Americas and Europe.

On the other hand, inventories were reduced by 20.4 billion yen from the previous fiscal year-end to 244.4 billion yen, and through reviewing some capital investments, we secured a positive free cash flow of 19.7 billion yen.

Although these results were challenging, we believe that the results of our efforts toward structural improvement, including the improvement of sales prices, eduction of proportional expenses, control of fixed costs, and compression of assets including inventories, are steadily appearing in the business environment where market conditions continue to be sluggish.

■FY2024 financial results

Outlook for FY2025: Key points

Regarding the business environment in FY2025, we expect the automotive market to slightly decrease compared to the previous year, and while the industrial machinery market will not achieve full recovery, we anticipate signs of recovery in some sectors such as robot gearboxes and machine tools. On the cost side, while prices of steel and other materials are stabilizing, labor costs and logistics costs are expected to continue rising, which will impact our business. Amid this business environment, our Group will continue to work on the improvement of sales prices while advancing value chain reform from upstream to downstream, including design, procurement, and production, to steadily reduce costs.

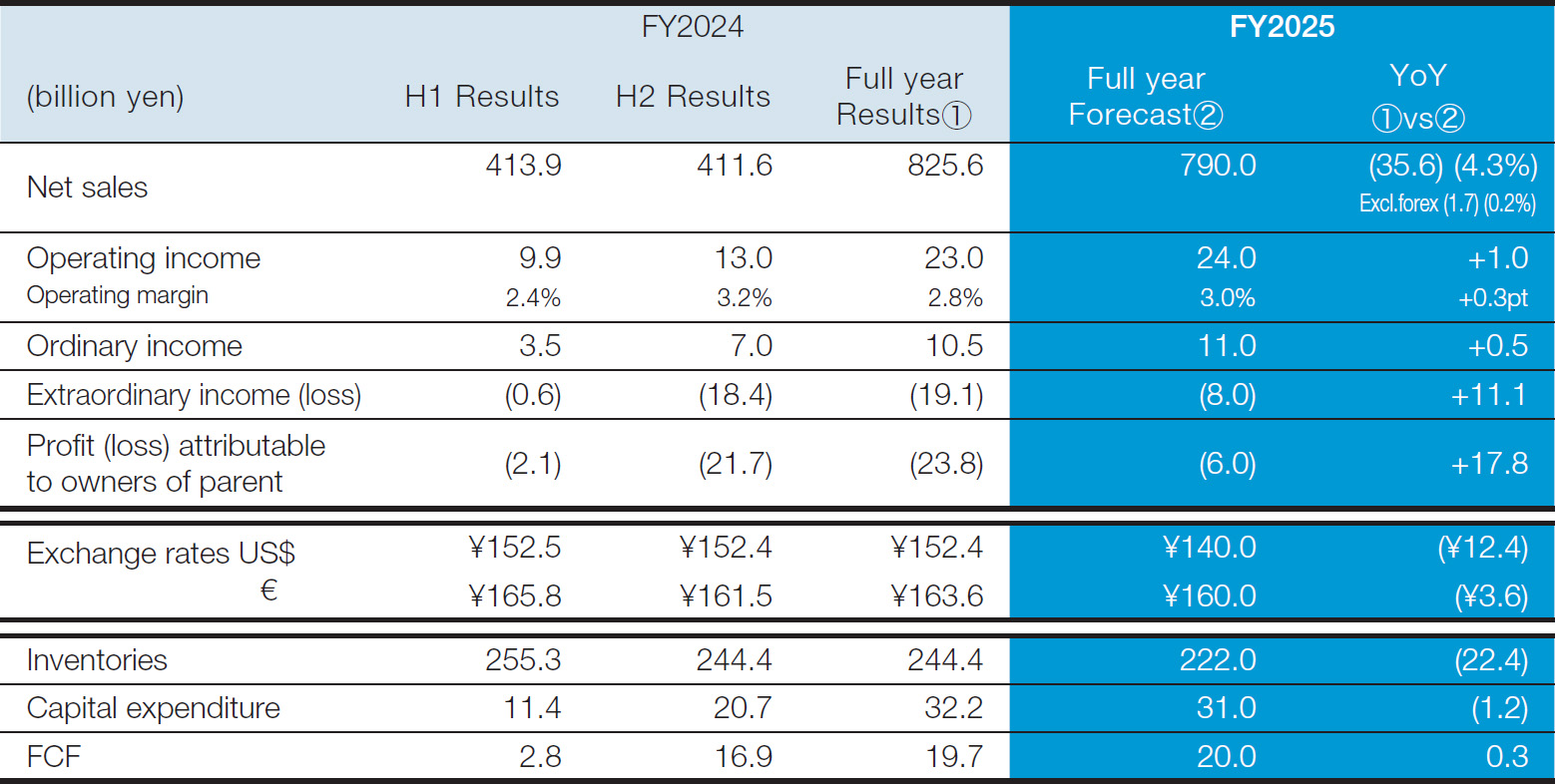

For FY2025, we expect net sales of 790.0 billion yen (down 4.3% from the previous year), operating income of 24.0 billion yen (up 4.5%), operating margin of 3.0%, and ordinary income of 11.0 billion yen (up 5.0%). We also continue to incorporate extraordinary losses of 10.0 billion yen as structural reform costs in Japan, the Americas, China, and other regions, with extraordinary losses of minus 8.0 billion yen and net loss attributable to owners of parent of 6.0 billion yen*1.

- Exchange rate assumptions: 1 USD = 140 yen, 1 EUR = 160 yen.

Inventories are expected to be 222.0 billion yen, a decrease of 22.4 billion yen from the previous fiscal year-end. Capital expenditures are expected to be 31.0 billion yen, a decrease of 1.2 billion yen from the previous year. Free cash flow is expected to be a positive 20.0 billion yen, similar to the previous year.

■Forecast for FY2025

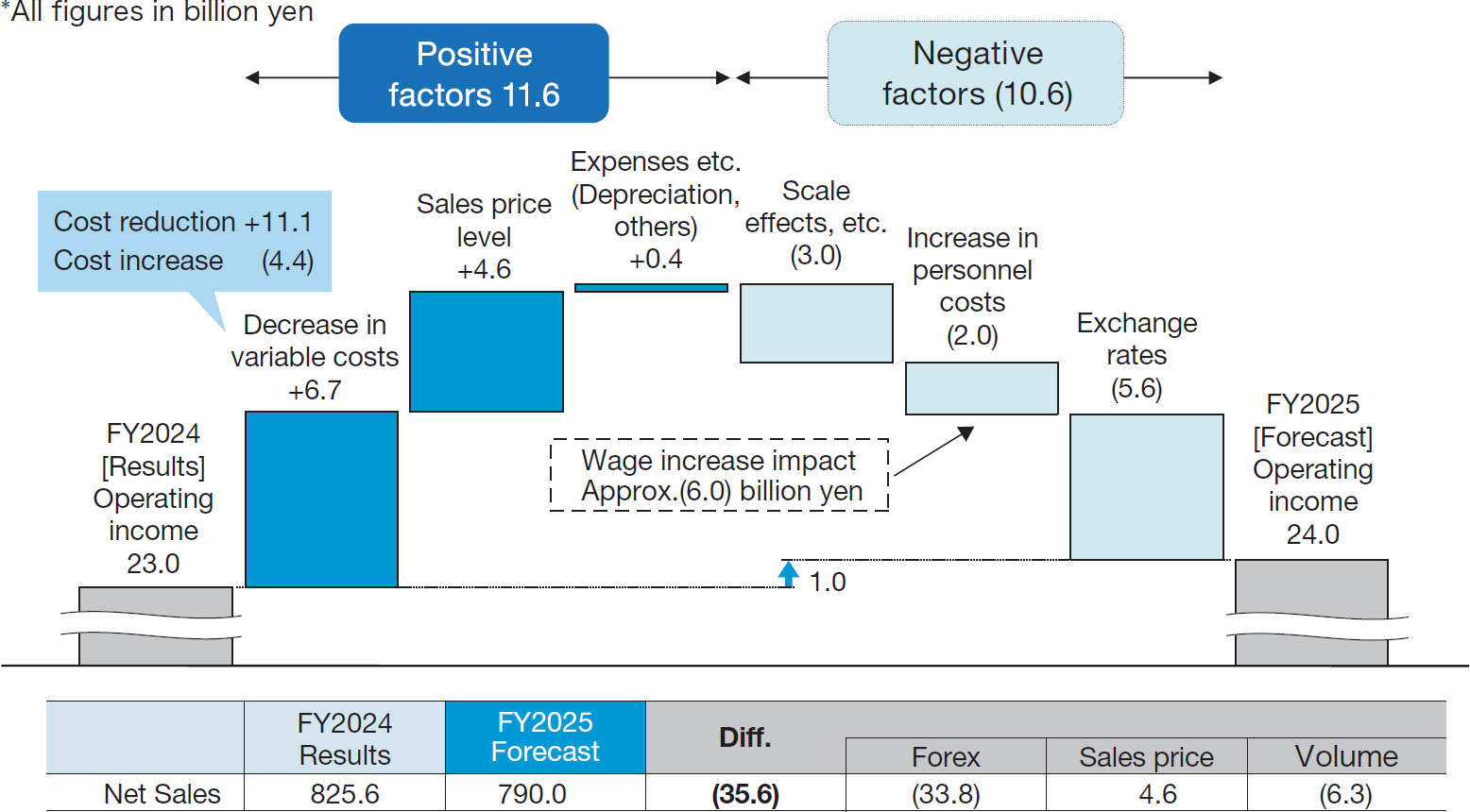

Factors contributing to changes in operating income

First, regarding factors contributing to profit decline, we expect a 6.3 billion yen decrease on a volume basis for declined sales and a 3.0 billion yen negative impact from reduced scale due to production cuts etc., as market conditions continue to remain sluggish.

In addition, personnel costs are expected to increase by 6.0 billion yen mainly due to base increases in Japan, for a total of minus 2.0 billion yen, despite the effects of structural reforms and headcount reductions due to the decrease in the workforce.

Regarding foreign exchange impact, we expect a negative impact of 5.6 billion yen as we assume a stronger yen this fiscal year compared to the previous year's results.

On the other hand, as factors contributing to profit increase, we expect variable cost reduction of 6.7 billion yen, improvement of sales prices by 4.6 billion yen, and expense reduction of 0.4 billion yen.

Regarding variable costs, in addition to the continued development and expanded use of competitive suppliers, the results of our value chain reform initiatives—which involve reviewing design and materials with ideas that are not bound by conventional thinking while still meeting customer requirements—are expected to achieve high-level cost reduction similar to the previous year.

Regarding the improvement of sales prices, while there is a reaction to the stabilization of steel prices, we will continue to pass on increases in labor costs and other factors, as well as improve sales prices for unprofitable businesses.

Regarding expenses, while we have incorporated costs for equipment maintenance and other factors, we expect fixed cost compression from structural reform being implemented in each region.

■Changes in operating income for FY2024 and FY2025

Progress of the Medium-term Management Plan “DRIVE NTN100” Final — Improving earning power

To build a corporate structure that enables our Group to achieve sustainable growth, it is essential to improve our earning power (operating margin and asset efficiency). One of the major factors hindering this improvement in earning power is the excess fixed assets that have resulted from past investments that no longer match the current market environment.

Structural reform to reduce excess fixed assets entails significant pain, but we are determined to complete it within the current Medium-term Plan period without passing it on to the next generation.

Progress of structural reform

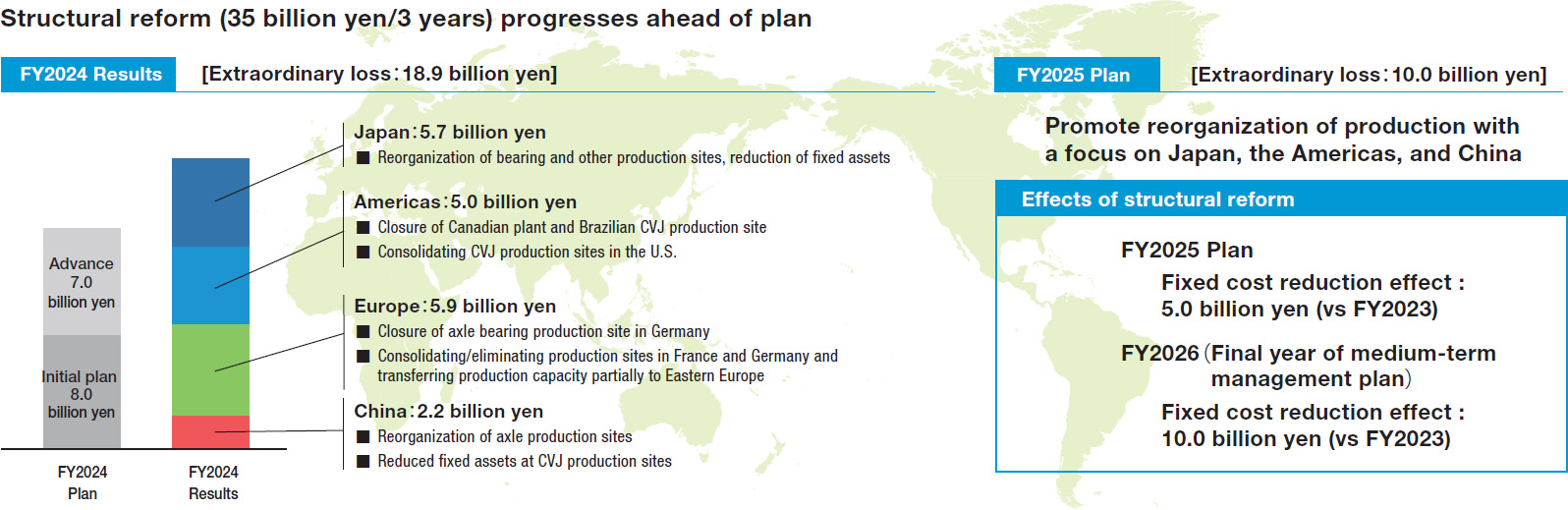

The NTN Group anticipates extraordinary losses of 35.0 billion yen in total over the three-year period from FY2024 to FY2026 as costs for structural reform.

In FY2024, we recorded extraordinary losses of 18.9 billion yen due to the acceleration of plans at some locations. In FY2025, we expect extraordinary losses of 10.0 billion yen in Japan, the Americas, China, and other regions, but there is no change to the three-year cumulative amount of 35.0 billion yen.

By region, structural reform in Europe and China is progressing almost as planned.

On the other hand, in Japan and the Americas, we are implementing not only simple structural reform such as factory closures, but also comprehensive reforms including production site transfers accompanying fundamental supply chain reviews.

As a result of such structural reform, we expect fixed cost reduction of approximately 5.0 billion yen in FY2025 (compared to FY2023). At the same time, from a BCP perspective, we are promoting dual source procurement with diversified supply routes. For example, we are establishing a system to procure materials from India and other countries in addition to China, while obtaining customer approval.

Going forward, we will continue to respond to unpredictable external environmental changes with speed and flexibility, while steadily advancing structural reform to complete NTN's revitalization.

■Progress of structural reform

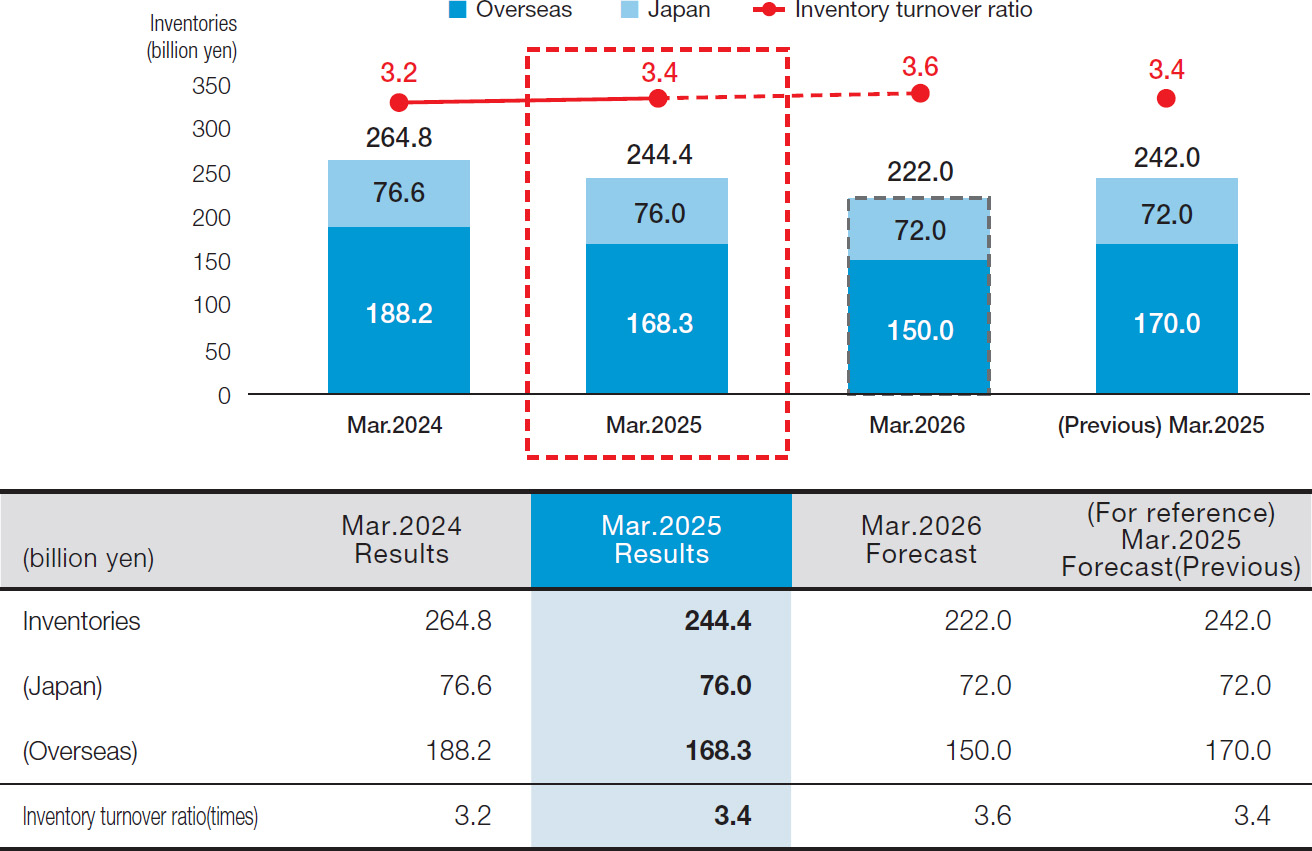

Inventory reduction

Another important point for improving asset efficiency is inventory reduction. Inventories have been increasing in recent years, mainly work-in-process inventory, due to supply chain disruptions caused by semiconductor shortages and other factors.

In FY2024, while continuing to expand inventory of popular products necessary for expanding aftermarket business, we reduced inventory stagnating in the supply chain, such as work-in-process inventory between factory processes, work-in-process inventory in transit, and inventory at overseas factories, through deepening production reform activities that have been ongoing at domestic manufacturing sites and expanding them to overseas manufacturing sites.

Inventory balance at the end of FY2024 was 244.4 billion yen, a decrease of 20.4 billion yen from the previous fiscal year-end, and the inventory turnover ratio was 3.4 times, the same as the announced figure.

We expect inventory balance at the end of FY2025 to be 222.0 billion yen, a decrease of 22.4 billion yen from the previous fiscal year-end, and the inventory turnover ratio to be 3.6 times, an improvement of 0.2 times from the previous year. Going forward, we will continue to reduce inventories and improve the turnover ratio, leading to improved earning power.

■Inventory trends and outlook

Toward building a corporate structure that can sustainably generate profits that exceed capital cost

Due to the deterioration of the external environment, including the prolonged Ukraine war, the worsening Middle East situation, and the impact of US trade policy, our current sales scale has significantly decreased from the assumptions at the time of formulating the Medium-term Management Plan.

We view the current reduction in sales scale as an opportunity to strengthen our corporate structure, and will accelerate structural reform activities while steadily implementing measures that contribute to improving the operating margin, such as “expansion of aftermarket business,” “improvement of sales prices,” and “reduction in variable cost through value chain reform,” as well as compression of inventories and fixed assets.

On the other hand, we will allocate the cash we generate to research and technological development in growth areas such as EV and electrification, services and solutions, as well as investments in achieving carbon neutrality, labor-saving measures, and digital transformation. We also plan to repay a certain amount of debt to enable diverse fundraising under favorable conditions in the future, while implementing stable and continuous shareholder returns.

With all Executive Officers working together, we aim to achieve 8% ROE in the final year of “DRIVE NTN100” Final and early achievement of 10% in the next Medium-term Management Plan, striving to build a corporate structure that can generate sustainable profits that exceed capital cost. We ask for the continued support and encouragement of all our stakeholders.